Im Buying an investment property is similar to buying a business; it needs to cash flow. Would you buy a business that loses money on a monthly basis? Probably not and you shouldn't buy an investment property that negative cash flows.

Now that we agree cash flow is critical, what should you do with the monthly cash flow surplus?

Let's assume the property cash flows after expenses and reserve fund allocation, $500. We encourage our clients to allocate a minimum of 8% of rental income for repairs, maintenance and vacancy allowance. For a property that generates $3,500 monthly, $280 is set aside.

There are 2 options to consider for the net $500 monthly cash flow:

1. Prepay investment property mortgage

2. Prepay principal residence mortgage

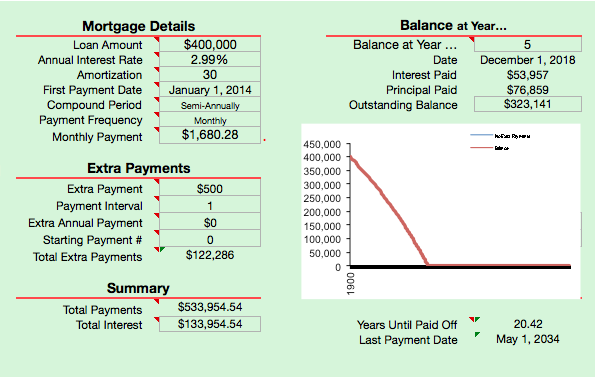

Assume your principal residence mortgage balance is $400,000 borrowed at 2.99% and amortized over 30 years with a monthly payment of $1,680.28. By diverting $500 monthly into your principal residence, the mortgage amortization is reduced to 20.42 from 30 years, saving you 9.6 years or $193,568 of mortgage payments.

Imagine having no mortgage payment!

Another factor to consider is tax efficiency (disclaimer: consult a professional accountant for tax advice, we are not accountants). The interest portion of a principal residence mortgage, for majority of homeowners, is not tax deductible. Whereas the interest portion of the investment property mortgage is tax deductible. A sound financial strategy is to pay off non tax deductible debt first.

Once the principal residence mortgage is paid off, use the rental property surplus to pay down the investment property mortgage to increase cash flow and pay it off ahead of the original amortization.

Questions? We can be reached via email or social media.